Overview

SMB lenders can reduce borrower friction by eliminating questions within their onboarding application and verifying business identity automatically from government sources. Friction in SMB lending has two sides: what borrowers experience at application, and what underwriters work through after submission. The highest growth SMB lenders are able to reduce friction for the borrower and their own underwriting teams without increasing risk exposure. Middesk accelerates credit and underwriting reviews for businesses, by automating data pulls across 400+ government and alternative sources, returning a structured business identity profile in seconds, and allowing lenders to review people and business-level risk in one view.

In brief

- Friction in SMB lending has two sources: information borrowers are asked to submit that lenders can retrieve independently, and time underwriters spend assembling data across disconnected vendor systems. Fixing one without the other means that friction is still in place.

- Automated business identity verification eliminates most front-end document requests. A unified, decision-ready underwriting file eliminates most back-end assembly time.

- Middesk handles both in one workflow — verification, lien data, person-level risk checks, and post-decision monitoring through a single API.

Choosing how to handle business identity verification in an SMB lending flow is a decision about how much friction to take during application, review, and funding. That friction determines the revenue a lender can generate from its business-line products and the operational efficiency the underwriting team can sustain as volume grows.

Some providers focus narrowly on making the borrower-facing application shorter. However, that still creates delays and friction for the borrower if a lengthy manual review is needed. The borrower experience is indeed faster but it won’t be for the underwriter. If the time-to-decision isn’t reduced, applicants drop off waiting for a response.

Here's how to address both sides.

Where does SMB borrower friction come from?

The standard SMB lending application asks borrowers to submit documents that are already on file with a government agency. Often the borrower doesn’t have or even know where to get these, adding incredible frustration instead of a streamlined customer experience. At Middesk, we believe that asking borrowers to upload what you can retrieve yourself is a lost opportunity. Credit risk information that goes beyond basic identity is available through UCC liens, federal and state tax liens, bankruptcy filings and civil judgments.

What you may still need to evaluate in an SMB borrower is a smaller set of data, such as financial details or context about their business and seasonality that can't be sourced independently. The onboarding process is reduced to a simple experience where the borrower deals with questions that they already have the answers to.

Ask providers directly:

- What data points does your platform retrieve from primary government sources at the time of application — without any borrower input?

- What's left for the borrower to submit, and why can't it be retrieved automatically?

- How current is the returned data? Is it a real-time pull from the source, or a cached result from a recent batch refresh?

What does automated business identity verification replace for lenders?

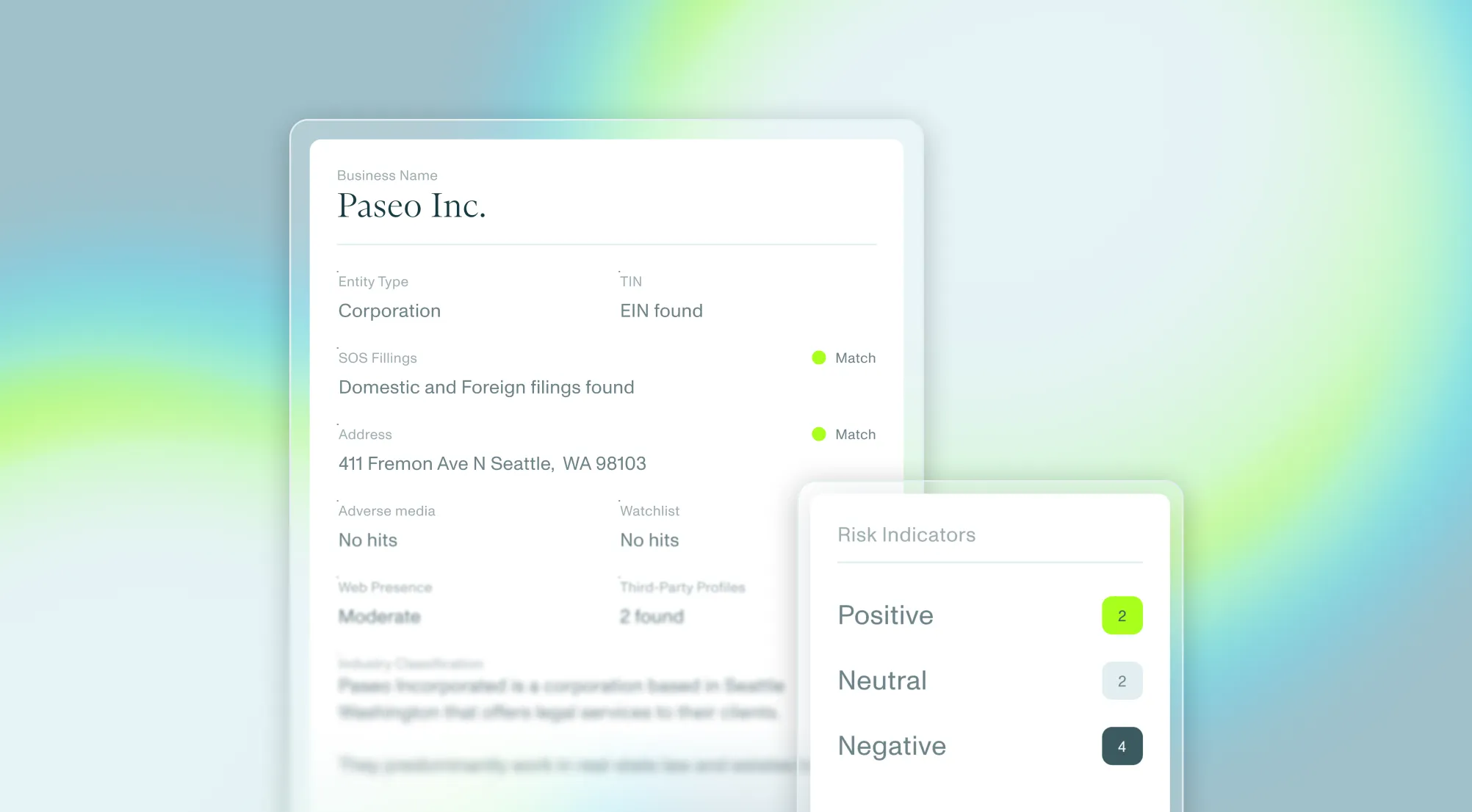

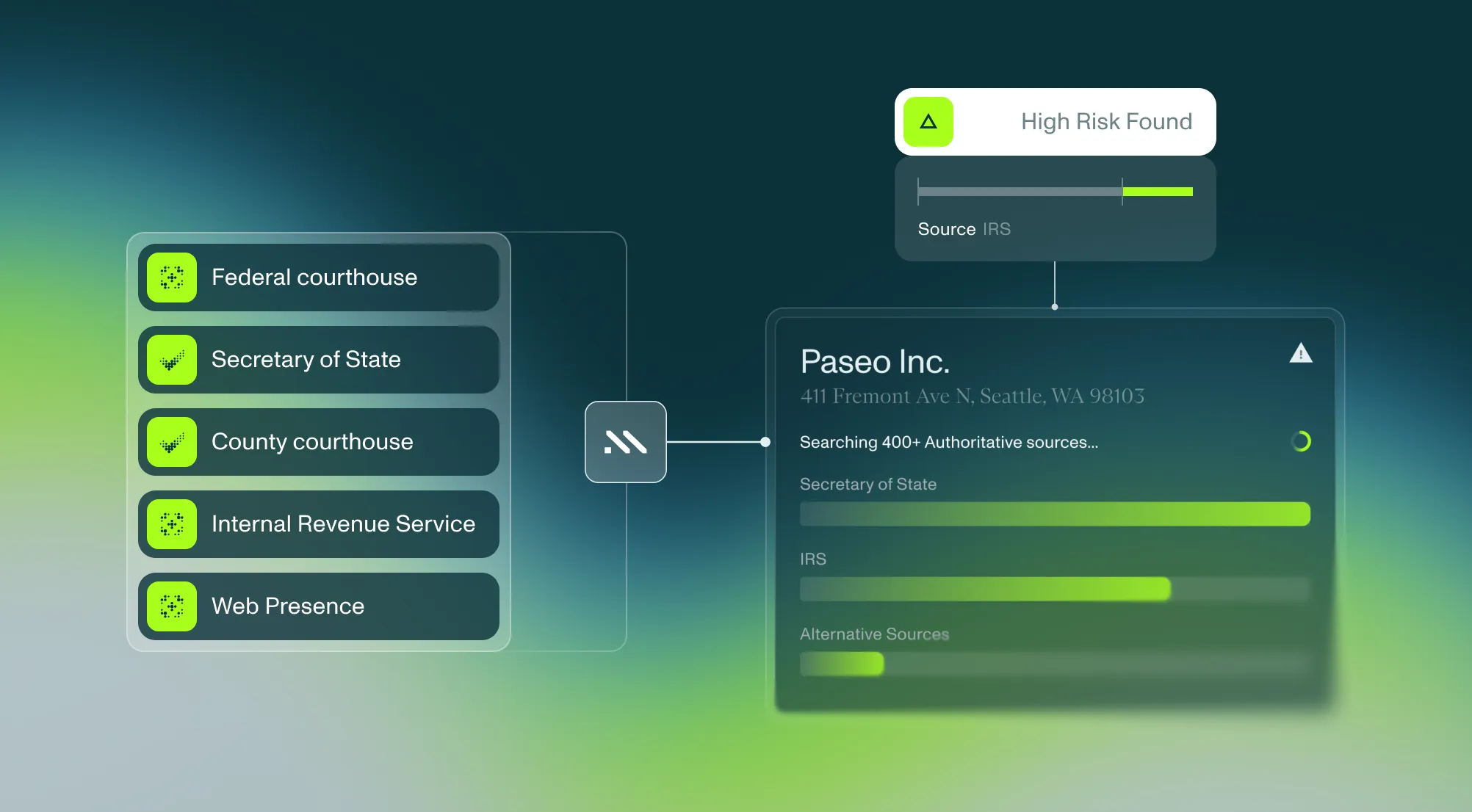

Automated business identity verification replaces the data and document collection step for most application data points and returns a structured profile that can accelerate the lender’s decisioning. Automated business identity verification also provides improvements in data quality that benefit the borrower. Middesk offers real-time data pulls from more than 400 government sources, which reflect the current state of an entity upon verification. 92% of Middesk’s records are refreshed within the past 10 days.

A lender can increase its ability to confidently review applications by getting documents straight from the source, rather than waiting for a borrower to submit them.

How to build a lending flow that reduces friction on both sides

In a well-structured SMB lending flow, business verification runs early in the application process, and fresh data is pulled in seconds so lenders are able to read application information and contextual information like lien, bankruptcy, litigation, and other credit-risk data in a file all at the same time. If this system is set up correctly, the result is that underwriters spend less time investigating and more time making decisions.

The decision structure that works best has three tiers: auto-approve for applications that clear all thresholds with clean signals, auto-decline for applications that fail hard policy criteria, and a review queue for the cases in between. The goal is to maximize the first tier, and enable the analysts to efficiently minimize the third.

Policies built on specific, data-driven criteria help decision making more effectively than those that end up routing ambiguous cases for analyst review because the system can't decide. Auto-approval policies need to be explicit, documented, and auditable for sponsor bank or compliance review. Partnering with an established partner like Middesk who has helped many high volume SMB lenders optimize their workflows is key to getting this right.

When evaluating lending flow architecture and data providers, ask providers directly:

- Can you configure which signals trigger auto-approve, auto-decline, and manual review?

- Is that logic auditable and adjustable without an engineering change?

- Can you see entity verification, lien data, and person-level risk in one place before the decision is made?’

Does speed add more risk to underwriting stacks?

The persistent assumption in SMB underwriting is that speed requires accepting more risk. That assumption came from an era when fragmented data meant faster decisions were incomplete decisions. A consolidated underwriting file changes the tradeoff.

In SMB lending, the person and the business are often inseparable. A business entity may carry clean credit signals while the owner, guarantor, or sole proprietor behind it carries personal UCC liens, prior bankruptcies, or outstanding judgments that the entity search never surfaces. In order to reduce friction on both the borrower and lender underwriting teams, business verification and people risk checks should live all on the same record.

Middesk's People UCC Lien Search runs those checks on submitted owners, guarantors, and sole proprietors in the same API call as the business verification, so the underwriter sees the complete business-and-person picture in one file.

Making the decision

Addressing friction in SMB lending requires being specific about where it lives. The borrower-facing application is the visible part, but the underwriting process is just as important.

Build the stack that handles both sides. Automate what can be retrieved from primary sources, consolidate the credit-risk checks for business and the people associated with them so they arrive in one file before a decision needs to be made.