Overview

In brief:

- UCC lien monitoring is a critical KYB process that helps companies understand the risk profiles of the companies they do business with

- Banks, credit unions, fintechs have a lot to gain from using lien monitoring solutions

- UCC lien monitoring works best when it’s part of a broader KYB and business verification system and process

If you’re a lender, you know that you need to be careful about who you extend capital to if you want to recoup your loan. For this reason, loan origination and UCC lien monitoring solutions are a vital tool for businesses that engage in lending.

Let’s dive right into what UCC lien monitoring is, and why it’s essential for financial institutions, particularly lenders.

What is UCC lien monitoring?

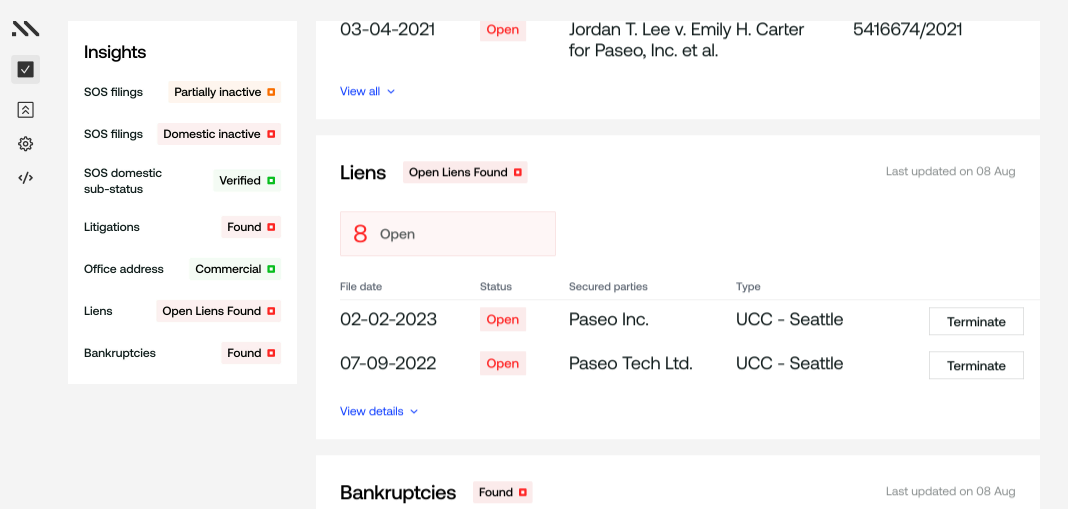

UCC lien monitoring is a risk management process performed by lenders, banks, and other financial institutions to determine whether a business they are trying to onboard or already work with has a lien registered, amended, or terminated. This is typically done through manual UCC lien searches, reviewing business information databases like the Secretary of State (SOS), but can be automated through monitoring, which uses a tool to automatically search these databases and notify the business if the business is connected to a lien.

By getting timely alerts on when a UCC lien is registered, amended, or terminated, companies can better manage their business relationships, effectively protect against undue risk, and extend capital with confidence.

Why is ongoing monitoring for UCC liens important to KYB?

Company’s risk profiles aren’t static — they change over time. While onboarding is a crucial component of risk management, it’s only a single snapshot in time for the companies that you do business with.

Just because you onboard a business today, that doesn’t mean they’ll remain in good standing forever. Business lien searches allow you to check for liens filed against a company. Automated lien monitoring ensures you get updated when there’s a change, so you can adjust the businesses risk profile accordingly.

Changes don’t always mean increased risk though. In some cases, changes to a lien filing status can actually reduce risk, potentially opening the doorway to extend more capital or even engage in a business relationship.

What kind of businesses need ongoing UCC lien monitoring?

Any financial businesses that have onboard business customers benefit from a UCC lien monitoring tool, as it helps these companies assess lending risk. These are the main types of businesses that need a lien monitoring solution:

- Banks - Traditional banks rely on lien monitoring to ensure the businesses they work with are in good standing and have a manageable, low risk profile.

- Lenders - When you’re responsible for extending capital to other businesses, you’ll want to be confident that you recoup your initial loan amount. Having a robust UCC lien monitoring system ensures you can extend capital with absolute confidence.

- Fintechs - Modern fintechs stand out by offering expedient, streamlined service that’s directly at their customers fingertips. Fintechs need to make sure they’re running adequate lien checks without causing too much friction in their onboarding process.

- Payment Providers - If you’re processing business payments, you’re responsible for not only what likely amounts to large sums of money, but you’re also responsible for the businesses reputation. Having adequate lien monitoring is critical to ensure safety.

- Marketplaces - Online marketplaces need to keep customers and merchants safe when shopping online. Perpetual and ongoing KYB monitoring is critical to maintaining trust on marketplace platforms.

Related content: Find out how to leverage UCC liens for effective business underwriting with your BEV Break Rewind.

How to set up UCC lien monitoring within your KYB process

It’s all about finding the right fit for your organization, providing adequate lien monitoring so you can lend your business clients capital without any worries. Let’s go over how to set up UCC lien monitoring in a KYB context—step-by-step.

Step 1: Determine what you need to monitor

First, you’ll need to decide exactly what you plan on monitoring, and which businesses it applies to. Do you need monitors set up on every business? Is it just specific businesses that meet certain risk criteria?

Then you need to consider if it’s just lien filings you care about. Do you also need to be aware of bankruptcy filings? Changes to a business’ EIN? What about updates to a watchlist status?

By determining what data you actually need to monitor and how lien monitoring works, you’ll be better able to decide which tool enables your team.

Step 2: Choose how often you need to monitor

Decide how often you want to check the lien filing status for the companies you work with. Is this something that only needs to be done monthly, quarterly, or even annually? Or is this something that needs to be monitored in real-time.

From there, you can decide whether you’re able to conduct monitoring by manually choosing which companies you want to check or automatically getting alerts for all businesses.

Step 3: Research and compare UCC lien monitoring tools

Check for tools that include UCC lien filing capabilities, helping you not only meet KYB requirements, but effectively assess risk before providing loans to businesses. Critically, check how often they refresh data, as this will directly indicate how accurate and useful your lien monitoring is.

If they only update their records every month, you’re stuck relying on outdated information. That rate of updates may be fine for your team, if you only plan on updating your records periodically. But this will be woefully inaccurate if you want more frequent updates or real-time data. And when you’re talking about notifications on liens or bankruptcy, taking action quickly can be the only way to protect your exposure to these risks.

Understanding your needs at this stage will help you determine if you’ll need an API monitor or if you’ll be able to manage it with a dashboard solution.

Step 4: Integrate the tool into your KYB tech stack

Now that you’ve made your choice, it’s time to integrate your UCC lien monitoring solution into your KYB tech stack. You’ll need to test it to make sure it meets your needs. Set up monitors on all the individual businesses you need perpetual KYB on or automate it for all businesses. This will ensure your lien monitoring works well as part of your existing KYB processes.

Step 5: Establish guidelines for how to act on a monitor

Outline clear, written guidelines that define how team members should act on alerts. What happens when you receive a monitor notification? Who on the team acts on it? What are their next steps? How does it affect current customers versus ones in the onboarding funnel?

With explicit guidelines for each scenario, you’ll be able to process alerts quickly and efficiently — without delays.

Step 6: Determine when a new monitor should be set up in the future

Now you need to decide when you’re going to implement monitors. Is it for all customers in all cases? Or do you want to select the businesses you monitor based on their individual risk profile?

3 best practices for monitoring liens in a risk-based KYB program

While it’s relatively straightforward to monitor for liens with the right system, there are a few best practices you should follow for success.

1. Centralize documentation

Having clear guidance on how to handle lien monitoring is crucial. This means establishing strict processes for your team members to follow for the lien monitors you set up. How do they handle each alert and what are the next actionable steps?

You also want to establish what conditions warrant the creation of a new monitor, so you know what you need to focus on in terms of your risk assessment priorities, and what you don’t need to allocate additional resources to.

2. Set a clear monitoring cadence

Decide how often you plan on monitoring for liens, and set a strict cadence that you’ll follow.

This doesn’t mean everything is set in stone, and you shouldn’t be afraid to change this cadence based on what your business demands. Just because you start out by setting up only specific monitors for companies individually doesn’t mean you can’t later expand the number of monitors you have on each company and increase the frequency at which you update data.

3. Seamlessly integrate lien monitoring with other due diligence processes

With the right tool, lien monitoring isn’t a stand alone solution. It’s a part of a broader business verification solution that lets you conduct essential KYB checks and meet compliance requirements.

When leveraged together, it helps you paint a clear picture of risk associated with the companies you do business with.

Related content: Find out where you can get lien data report information on businesses for KYB.

Top 4 UCC lien monitoring services & tools

To help you track UCC lien filings and effectively manage KYB risk, we dive into some of the top UCC lien monitoring tools on the market.

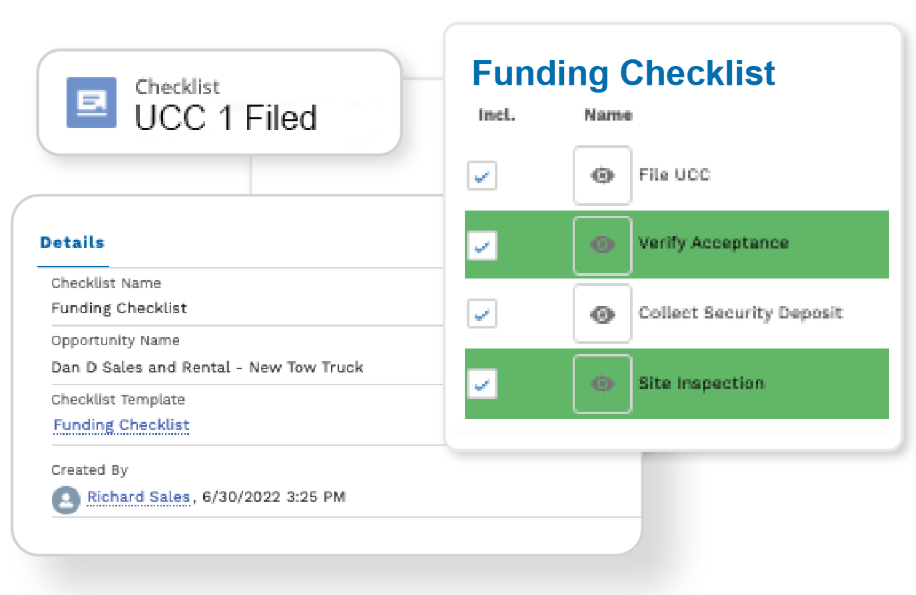

1. Middesk: best for lending risk assessment

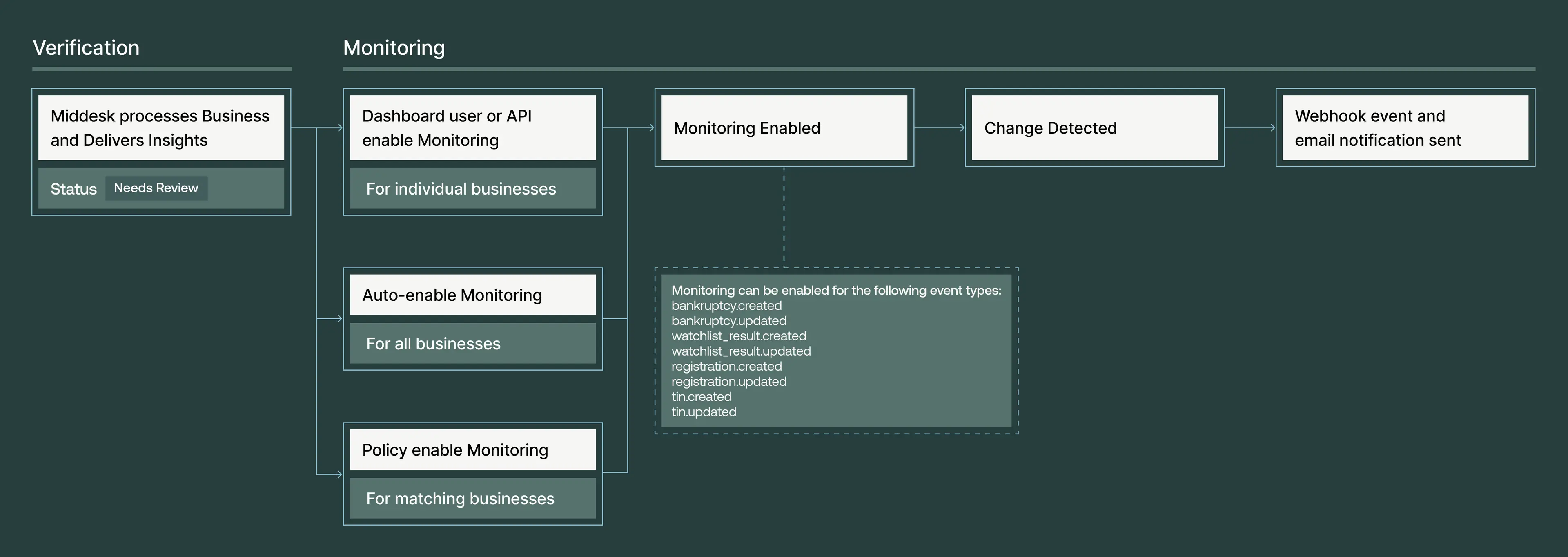

As part of Middesk’s business verification suite, we offer UCC lien monitoring capabilities, helping you effectively manage — and mitigate — risk. Middesk Monitor works by tracking whether a business you are monitoring has a change in their status, and can track this for UCC liens, as well as for bankruptcy, watchlists, TIN/EIN changes, and SOS business registration changes.

As part of Middesk’s business verification suite, we offer UCC lien monitoring capabilities, helping you effectively manage — and mitigate — risk. Middesk Monitor works by tracking whether a business you are monitoring has a change in their status, and can track this for UCC liens, as well as for bankruptcy, watchlists, TIN/EIN changes, and SOS business registration changes.

Middesk lets you individually dictate which businesses you want to track. You can even control the exact monitors you want to set up. This lets you cut out the noise for low-risk entities and focus on the alerts that actually matter. Alternatively, you can automate with our API, or even track all businesses and set up all possible notifications so you never miss a single thing.

2. MANTL: best for new digital account creation

MANTL is a consumer deposit and loan origination solution for banks and credit unions. They focus primarily on accelerative deposit growth, launching digital brands, and branch transformation, helping financial institutions navigate the shift to a more digital banking experience pioneered by fintechs.

MANTL is a consumer deposit and loan origination solution for banks and credit unions. They focus primarily on accelerative deposit growth, launching digital brands, and branch transformation, helping financial institutions navigate the shift to a more digital banking experience pioneered by fintechs.

3. Northteq: best for loan origination

Northteq simplifies and automates loan origination procedures, making it easy for your company to manage client lending. Streamline the process so clients can get quickly from application to funding.

Northteq simplifies and automates loan origination procedures, making it easy for your company to manage client lending. Streamline the process so clients can get quickly from application to funding.

Through Northteq’s partnership with Middesk, clients are able to verify customer identities within their platform, gaining access to other business verification details that help them assess risk associated with B2B relationships.

4. LoanPro: best for automated loan servicing

LoanPro is a long management software that offers loan origination and a collections suite that ensures you recoup your capital. Their commercial lending platform helps companies manage business loan management in particular.

LoanPro is a long management software that offers loan origination and a collections suite that ensures you recoup your capital. Their commercial lending platform helps companies manage business loan management in particular.

Middesk Assess lets you conduct reliable, automated risk assessments that let you underwrite with confidence. Get notified of key risk signals that help you filter out high-risk businesses early in the onboarding process.

WIth ongoing UCC lien monitoring, you get notified when businesses you work with have a lien filed against them, so you can adjust their risk profile accordingly — without delay.

Try a demo today to see how Middesk’s lien monitoring solution can help you effectively manage and prevent risk associated with lending.