Overview

In brief:

- Adding alternative credit data into your onboarding flow can help identify fraud slipping through the cracks

- Alternative credit data sources include things like web presence, IP address behavior, press, and social media

- You’ll need to conduct good research to find a quality alternative credit data provider

Lenders are increasingly relying on alternative credit data sources to build more robust risk scoring in business credit underwriting, but it’s challenging to identify exactly what kind of alternative credit data is useful in business onboarding vs what is just noise that overcomplicates your automated KYB process.

In this article, we’ll show you exactly how to find and use alternative credit data, and specifically where to integrate this step in your business credit underwriting onboarding process effectively. To do that, we’ll cover:

Let’s get started with the basics.

What is alternative credit data?

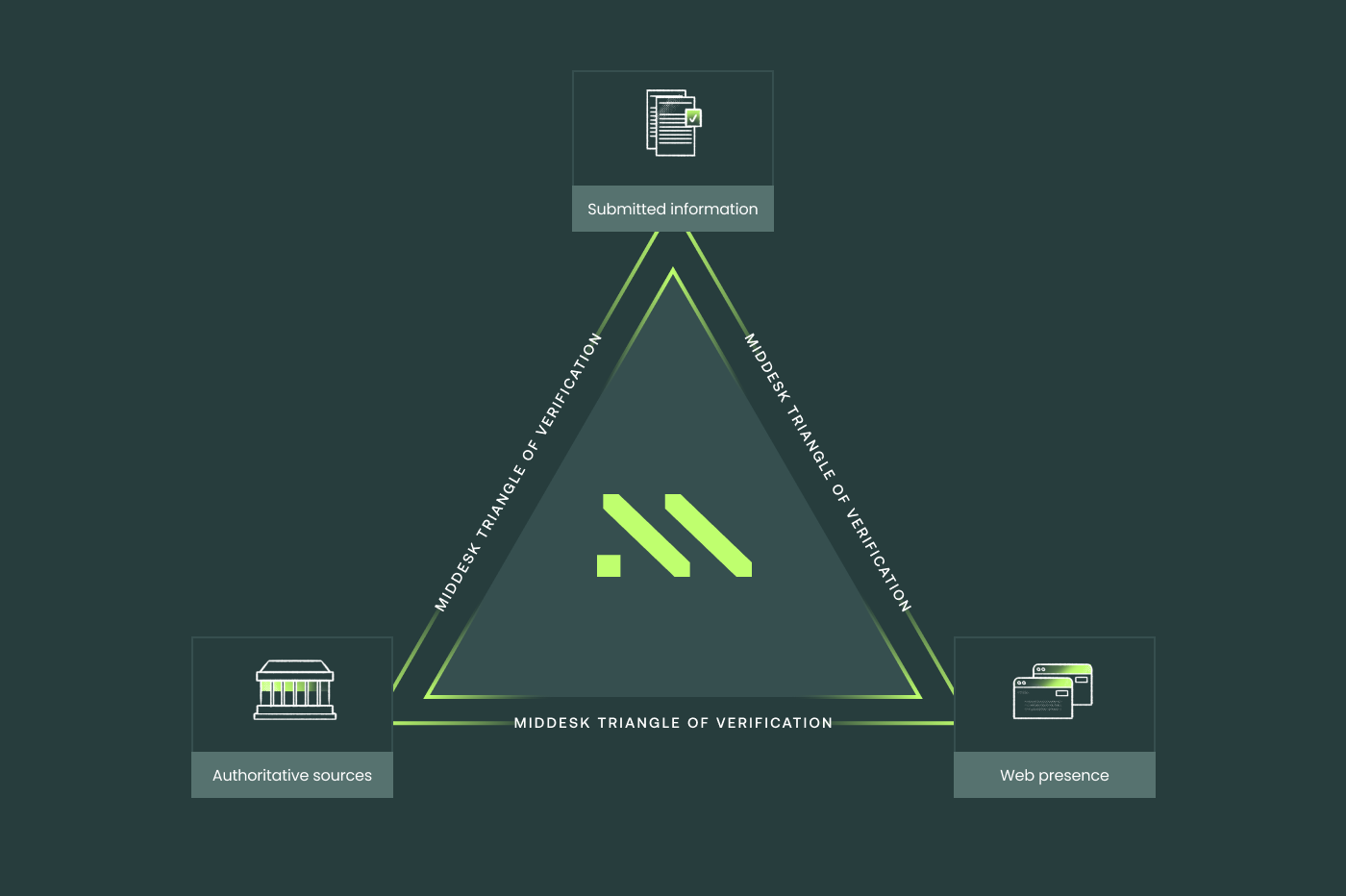

Alternative credit data is any data collected from outside the traditional regulatory systems used to help signal business identity, intent, or risk of fraud in business credit underwriting. It often includes things like press coverage, website presence, phone number and address consistency, and social media.

Alternative credit data is the opposite of authoritative credit data, which would traditionally include things like Secretary of State (SOS) filings, Employer/Tax Identification Numbers (EINs/TINs), or business licenses.

Both sources of data are key to building a robust credit underwriting risk scoring program. When it comes to Know Your Business (KYB), the strongest verification occurs when the information submitted to you by the business matches what’s in authoritative data sources, and matches what’s in alternative credit data sources.

This is the strongest indicator that the business you want to onboard is legitimate, while a lack of consistency across these three areas is your indication that some risk may be present.

This is the strongest indicator that the business you want to onboard is legitimate, while a lack of consistency across these three areas is your indication that some risk may be present.

What types of alternative data can be used for business credit underwriting?

Technically, almost anything from a non-authoritative data source could be used to enable business credit underwriting, but some of the most helpful sources of alternative data are:

- Adverse media and press mentions - Looking for negative mentions of the business in the news can help you identify potential risks like fraud or the breaking of regulations

- IP address behavior - Odd behavior from the IP address for the business can be an indicator of risk

- Website presence and metadata - The state of the businesses website, how polished it is, and how long it’s been there can all be indicators that help assess risk

- Business email or phone number consistency - Looking for the different numbers and addresses listed in any form of online presence for the business and comparing them to what you find in authoritative databases can help identify inconsistencies

- Social media - You can identify intent or activity of the business, sometimes finding indicators of potential risk

- Directory listings - When businesses list themselves online in directories like Google Business Profile, you can compare the information listed there to what you find in authoritative data sources to check consistency

- Online reviews - These can sometimes offer indications of issues with the business, bad practices, or even fraud and scams that are present

Related content: Find out why the best KYB strategies use both alternative and authoritative data sources.

What’s the difference between using alternative data and traditional credit scoring?

When using alternative credit data vendors vs traditional credit bureaus, you enhance your KYB program by including even more data to evaluate your prospective customers with. Alternative credit data isn’t a replacement for authoritative credit data, but rather a way to conduct Enhanced Due Diligence (EDD), and better score risk during credit underwriting and onboarding.

Is the alternative data used for credit scoring and business credit underwriting the same thing?

The alternative data that’s available for credit scoring and business credit underwriting would be the same, as any lender could find a way to access the alternative data available, and use it as needed.

The key difference would be using alternative data that’s helpful for your specific needs when underwriting—for example, lenders working directly with consumers rather than with businesses might utilize different data points to make their risk scoring decisions.

Using alternative data for business credit underwriting & lending

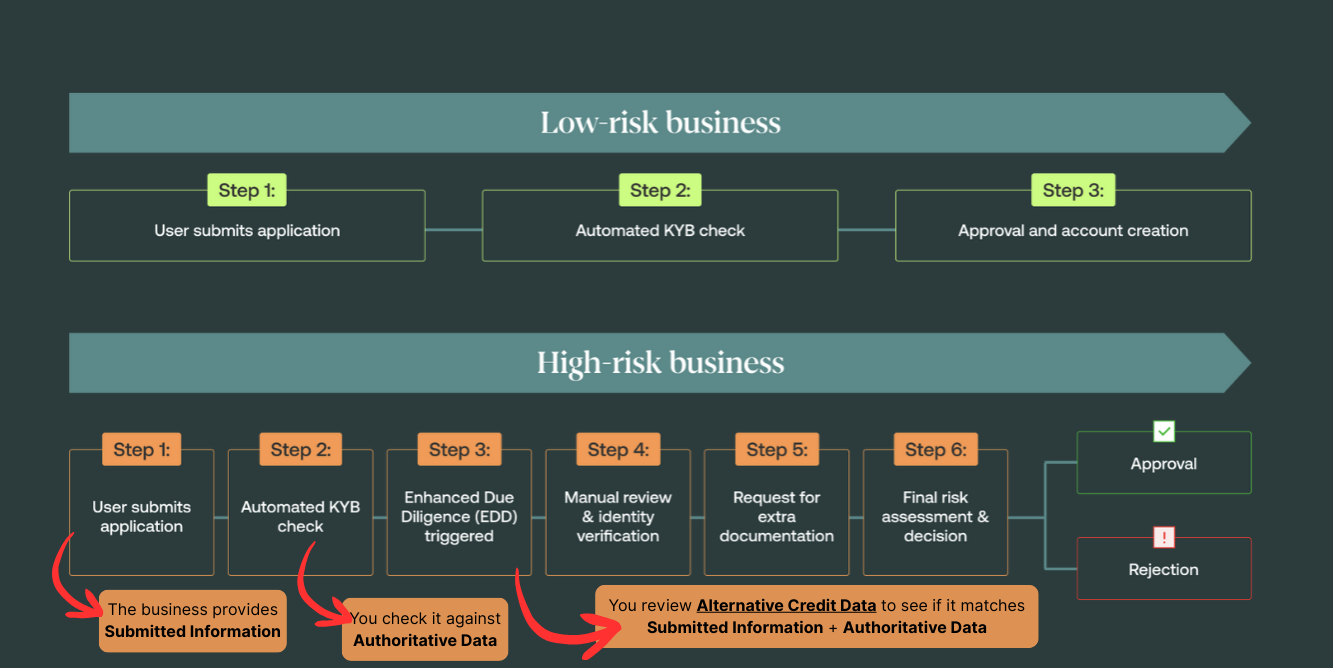

Understanding what data is available to you is only the first step. To integrate alternative credit data into your business credit underwriting onboarding process, you should follow these steps:

1. Business submits lending application

Your applicant submits their application, providing any requested documentation needed for you to conduct your KYB process. This should include any necessary documents for you to conduct risk assessment on the business, like EIN/TINs, SOS filing information, business formation documents, business name and address, etc.

At this step: You are collecting data directly from the applicant, the Submitted Information.

2. Automated KYB check using business verification software or API

Using your business verification tools and existing KYB process, you check what the applicant provided you against authoritative data sources to confirm the information is accurate, and look for early indicators of potential fraud or risk.

Your KYB software should be able to check the business EIN, pull state-specific SOS data, look for watchlist, sanctions, or PEP hits, and anything else you need to check against authoritative sources.

At this step: You are using Authoritative Data to confirm the Submitted Information.

3. Conduct Enhanced Due Diligence (EDD) using alternative credit data

Using any alternative credit data sources, check the information against the information to look for inconsistencies or red flags that might be indicators of risk. When the alternative credit data shows a difference from the information you have, it should trigger a manual review of the applicant, putting them into a high-risk onboarding flow.

A great example is the official business address, because it’s a very easy data point to review from all 3 sources. The applicant would provide you with one, the SOS state filing would have one, and you can usually find this in an online business profile. If all 3 match, that shows consistency, and if they don’t, it’s an indicator to look further into the applicant.

At this step: You are using Alternative Credit Data to verify that the Submitted Information and Authoritative Data information all match.

4. Manual review & identification verification

Once a manual review is triggered, you should put the applicant through a more rigorous flow including further checks with manual oversight from your team’s compliance leaders. When the automated software and data checks flag something to review, you should look into it further and see if you can determine where the inconsistency is coming from.

At this step: You are manually reviewing the inconsistencies that were flagged between the Submitted Information, the Authoritative Data, and the Alternative Credit Data,.

5. Request for extra documentation

Once you know what the issue could be, you can request further documentation from the applicant that clears up the inconsistencies. You can be specific here in what you need, having checked their submitted information again both types of data to not create further friction on customers who might have an honest inconsistency, while still ensuring the right checks are in place to identify a bad actor at this stage and prevent them from proceeding further through the onboarding funnel.

At this step: You are presenting the inconsistencies found from the Submitted Information, the Authoritative Data, and the Alternative Credit Data to the prospective customer, and requesting documentation that proves which is accurate.

6. Final risk assessment & decision

Once you receive the documentation needed from the prospective customer, you can further review it and make a final decision based on your assessment of the risk. Sometimes the inconsistency can be a small and insignificant error - like a business didn’t change the address on their website, even though it’s been changed in their business filings with the SOS. This would be a small risk inconsistency, and one you can verify with further documentation.

When the risk is greater, like if the newly submitted information doesn’t line up with any data sources you have checked it against, you can make a final decision to remove this prospect from the onboarding funnel.

At this step: You are reviewing Newly Submitted Information from the business, and further checking it for inconsistencies against Authoritative Data and Alternative Credit Data.

3 best alternative credit data sources for lending decisions

These are some of the best alternative credit data APIs and software platforms that can provide the lending-specific alternative data you need to conduct EDD in your onboarding flow.

1. Middesk

Middesk is a KYB verification tool that can automate the loan origination process to help you unlock capital for your customers faster. With a mix of both the authoritative data you need to be compliant (EINs, SOS filings) and the alternative data that provides deeper risk scoring insights (IP address behavior, adverse media), you get a robust tool with all data you need in one place.

Middesk is a KYB verification tool that can automate the loan origination process to help you unlock capital for your customers faster. With a mix of both the authoritative data you need to be compliant (EINs, SOS filings) and the alternative data that provides deeper risk scoring insights (IP address behavior, adverse media), you get a robust tool with all data you need in one place.

Middesk customers have seen a 31% lift in auto-approvals because of its direct pipeline into each state’s SOS database, and 92% of business records within our data was updated in the last 10 days, so you know both your authoritative and alternative credit data is as fresh as possible.

2. Northteq

Image Source: Northteq

Image Source: Northteq

Northteq offers the Aurôra Loan Original System (LOS), providing automated process flows to make lending easy. With Northteq, you can originate, score, decision, and document deals in minutes. Northteq even partners with Middesk to verify the identities of customers within the Northteq platform.

3. LoanPro

Image Source: LoanPro

Image Source: LoanPro

LoanPro offers loan origin data with a variety of datasets and integrations within its platform that allow you to evaluate alternative data sources. Built as an API-first platform, you can set up loan original verification automations to help speed up your process, while still having the resources needed to verify through alternative data sources.

How to evaluate providers for integrating alternative credit data into loan decisions

In addition to the comprehensive platforms like the ones we’ve listed above, there are other places you can look for alternative credit data - even by manually combing through social media or online press coverage.

But it’s important to make sure the data you are using meets certain criteria that enables you to actually make lending decisions with it. Here are some of the key things to look for in your data:

1. Freshness

The data should be frequently and recently updated, which ensures you can actually rely on it to make risk-based lending decisions. When it comes to credit data, knowing the information you’re reviewing is current—within days—is often critically important to detecting fraud in the onboarding process.

How To Evaluate This: Data Freshness & Monitoring Lag

2. Completeness

Data should be complete enough that you can make meaningful inferences with it, and actually make risk-based decisions using it. By qualifying the alternative data you are using, you can ensure it is bringing value to your risk assessment, rather than complicating the process unnecessarily.

How To Evaluate This: Fill Rate & Qualification Rate

3. Consistency

When it comes to credit data, values for the same business entity should be the same across all data sources, datasets, and data points. When you see contradictions or discrepancies, that’s when it’s essential to send prospective customers into a higher-risk onboarding flow.

How To Evaluate This: Anomaly Detection & Manual Inconsistencies

4. Uniqueness

Individual data records should not be duplicated within datasets, as this can lead to inaccurate risk scoring or false positives when it comes to identifying fraud.

How To Evaluate This: Duplication Count

5. Accuracy

Especially when utilizing alternative credit data to compare it against authoritative and submitted data, the accuracy of the data is critically important when gauging how much it aligns with the source of truth. Data should be free from errors, enabling better automation in your KYB process

How To Evaluate This: Error Rate & Auto-Decision Rate

We’ve put together a guide on how to run your potential KYB vendors through a data-driven test to make sure they can handle your precise needs.

What's next

CIP is our first workflow, but the full decision-making lifecycle across B2B relationships is next. We're building a complete orchestrator suite covering every business decision you make - from risk tiering and enhanced due diligence to creditworthiness, merchant onboarding, and fraud investigation.

The intelligence platform becomes infrastructure that thinks, investigates, and acts - handling the manual work so your team can focus on the work that only humans can do.

Get started

CIP workflow is available now in public beta for existing Middesk customers.

Contact us today to get a demo and explore our product offerings.