Overview

In brief:

- A risk-based approach to merchant onboarding is the best way to ensure fraud doesn’t make its way onto your platform

- Balancing this with smooth onboarding for your other merchants is key to establishing a trustworthy platform with legitimate merchants

- A merchant onboarding solution can help detect risk earlier (at the top of your funnel) to cut out wasted onboarding time on businesses likely to commit fraud on your platform

In 2023, Amazon reported that over 700,000 seller attempts on their platform were fraudulent. As online marketplaces continue to grow and offer more services, fraudsters find new and more clever ways to use marketplaces to commit fraud and take advantage of consumers.

As a marketplace, it is your responsibility to adequately assess the risk potential merchants pose to you before onboarding them to your platform, and conducting thorough KYB (Know Your Business) checks to ensure the business is legitimate, in good standing, and will help maintain the trust and integrity of your platform.

To do this, you need to take a risk-based approach to onboarding, and know how to adequately score the risk of potential merchants.

Let’s start by covering some of the basics about merchant onboarding and risk scoring.

What is merchant onboarding?

Merchant onboarding is the process of bringing a new merchant into your platform (like marketplaces), which requires KYB checks per U.S. regulations in certain industries. If you don’t conduct required checks during merchant onboarding, you open the door for bad actors to commit fraud on your platform.

You are required to collect and verify certain information about the merchants, including their business name and address. You would also need to verify the EIN/TIN of the business to determine if it is legitimate and in good standing with the IRS. And you need to ensure the business or people associated with it are not on any Watchlists, Sanctions Lists, or PEP lists.

Onboarding is simply the process of bringing a merchant on to your platform, but there’s much more to it than that, because some merchants post a risk to your platform and your business if you bring them on and they use your platform to commit fraud. You need to also conduct merchant risk monitoring to ensure you don’t open yourself up to these kinds of liabilities.

What is merchant risk monitoring?

Merchant risk monitoring is the process of scoring and assessing the potential risk a merchant poses to you prior to onboarding them, using a variety of factors based on your industry regulations. The risk assessment you conduct should consider how likely the merchant is to use your platform to commit fraud.

Your KYB process should include a step to assess the risk of a merchant and not onboard merchants that are high-risk.

What is considered a “high risk” merchant account?

A high risk merchant is one that’s determined to be more likely than a normal merchant to commit fraud, using the platform for things like chargeback fraud or synthetic identity fraud. During onboarding, platforms will often score a merchant based on its perceived risk of being fraudulent.

Certain aspects lead to this determination that a merchant is high-risk, including things like:

- Industry the operate in - Industries like adult entertainment, gambling, tobacco, or pharmaceuticals are often considered high-risk, for example

- Financial history - If they have a history of bad credit or bankruptcy

- Bad industry reputation or previous instances of fraud - Leads to the assumption that they may commit fraud again on a new platform

- Potential for high-ticket sales - This increases the potential liability you open yourself up to as the platform if those sales are fraudulent

- International operations or operating in multiple jurisdictions - These places can have different legal regulations and requirements, meaning what’s legal in one place may not be in another

- Merchant age - A newer on unestablished merchant may not be very trustworthy to onboard with further Enhanced Due Diligence (EDD)

Determining what is high-risk to your business without eliminating perfectly legitimate merchants is one of the most challenging aspects of merchant onboarding. Our eBook below can show you how to keep onboarding smooth without opening the door to fraud.

Learn how modern KYB balances security and customer satisfaction in business onboarding.

What is merchant account identity theft?

Merchant account identity theft is a type of fraud where the fraudster is onboarded onto a platform illegitimately by posing as a merchant. They obtain basic business information like EINs/TINs, business name, and address, and appear as though they are the merchant convincingly enough to get on the platform.

The fraudster then uses the platform to process transactions (pretending to sell real goods & services), is able to acquire the money from sales on the platform, and then leaves, never providing consumers anything in exchange for their money.

Warning! Most fraudsters who commit merchant account identity theft successfully are able to do it because the platforms they are onboarded to are not conducting thorough enough checks to ensure the merchant is legitimate prior to onboarding, or adequately scoring the risk of potential merchants before onboarding them, even when basic business information is verified.

A thorough merchant onboarding process is necessary to make sure this doesn’t occur on your platform, and U.S. regulations make this absolutely necessary for you to do.

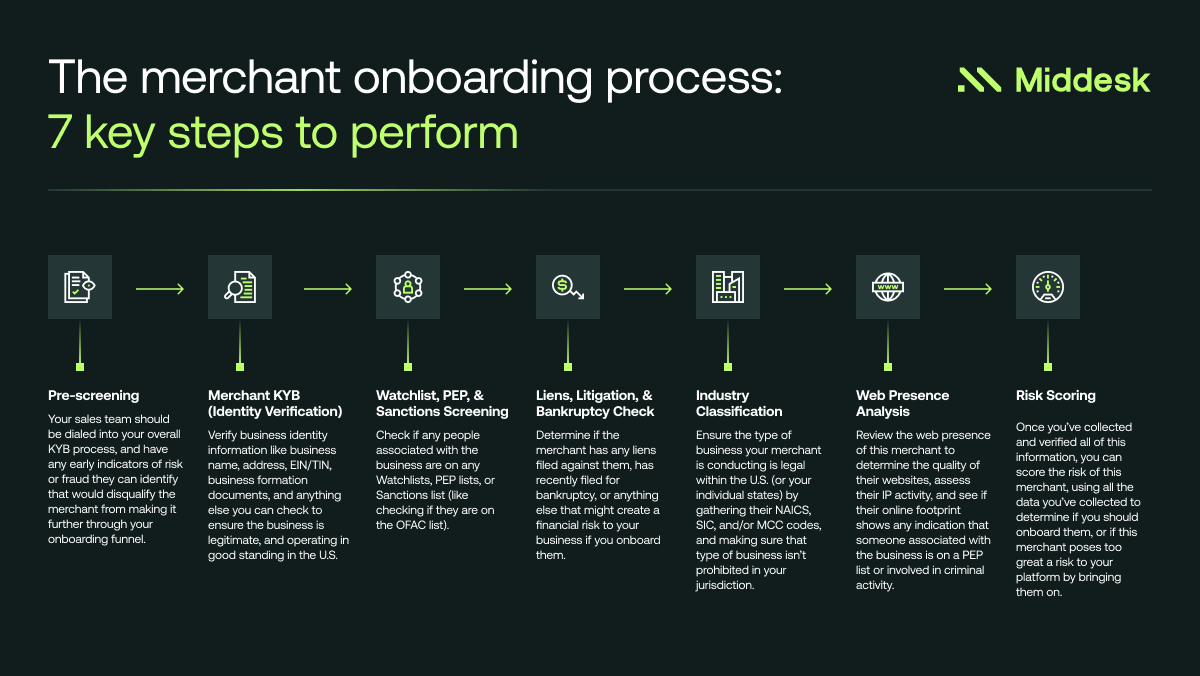

The merchant onboarding process: 7 key steps to perform

When onboarding a new merchant to your platform, you want to ensure your KYB process includes all 7 of these steps, as each check here can be an early indicator of risk during onboarding.

- Pre-screening - Your sales team should be dialed into your overall KYB process, and have any early indicators of risk or fraud they can identify that would disqualify the merchant from making it further through your onboarding funnel.

- Merchant KYB (Identity Verification) - Verify business identity information like business name, address, EIN/TIN, business formation documents, and anything else you can check to ensure the business is legitimate, and operating in good standing in the U.S.

- Watchlist, PEP, & Sanctions Screening - Check if any people associated with the business are on any Watchlists, PEP lists, or Sanctions list (like checking if they are on the OFAC list).

- Liens, Litigation, & Bankruptcy Check - Determine if the merchant has any liens filed against them, has recently filed for bankruptcy, or anything else that might create a financial risk to your business if you onboard them.

- Industry Classification - Ensure the type of business your merchant is conducting is legal within the U.S. (or your individual states) by gathering their NAICS, SIC, and/or MCC codes, and making sure that type of business isn’t prohibited in your jurisdiction.

- Web Presence Analysis - Review the web presence of this merchant to determine the quality of their websites, assess their IP activity, and see if their online footprint shows any indication that someone associated with the business is on a PEP list or involved in criminal activity.

- Risk Scoring - Once you’ve collected and verified all of this information, you can score the risk of this merchant, using all the data you’ve collected to determine if you should onboard them, or if this merchant poses too great a risk to your platform by bringing them on.

6 merchant onboarding best practices for a risk-based KYB approach

Trying to walk the line of not making onboarding so cumbersome for your legitimate potential merchants while also making sure you shut the door tight to potential fraud is very difficult. These best practices will help you with this balancing act, making sure your risk-based approach stops the biggest threats to your business at the top of your funnel.

1. Perform basic business identity checks at the top of your workflow

Collecting and verifying basic business information like name, address, and EIN/TIN, and checking that against the SOS databases can immediately tell you the business registration status of the merchant, as well as whether the information they gave you matches what’s in the IRS and SOS databases.

A quick check like this at the top of the funnel can weed out the easiest to spot fraudsters, and then doesn’t require further due diligence, cutting out time wasted digging into merchants that are obviously fraudulent.

2. Use segmentation to build cohorts through dynamic risk scoring

Use your checklist of high-risk merchant factors to segment your applicants into cohorts based on their risk profile. Your risk scoring system should be able to provide you with a comprehensive upfront score based on all factors so you can allocate your internal resources properly based on how high of a risk the potential merchant is.

You also want to use dynamic risk scoring that can assess the risk level of an applicant in real time so you can adjust the friction level necessary for the merchant based on their perceived risk.

3. Build an adaptive verification process for higher-risk merchants

An adaptive process means the criteria and what’s required of the merchant might change as they move through the onboarding workflow, depending on how they answer questions earlier in the process. For example, if a merchant answers onboarding questions that indicate they are likely to be a higher-risk merchant, they can then be required to provide additional documentation as they move through due diligence checks.

Low risk merchants who aren’t likely to commit fraud then would not have to continue through this due diligence process, and you can keep onboarding smoother and easier for them, as the things you are looking for wouldn’t apply to them.

4. Run whatever you can in the background to reduce friction

Rather than having your merchants continue to fill out paperwork, manually input information, and provide documentation, run your verifications in the background of the onboarding process where they can’t see it.

You can also automate a lot of the process by doing it this way, and keep human oversight where it needs to be — checking on things that demonstrate the need for further investigation — rather than doing manual work that can be automated.

5. Use a tool to automate this process and help you scale

Conducting these checks manually on every merchant trying to get on your platform does not work when you’re onboarding dozens or even hundreds of merchants each month, and it doesn’t scale with your business.

A KYB automation tool that can perform these business verification checks on each merchant that enters the funnel can typically save you hours per merchant, freeing up a lot of internal resources for other aspects of KYB or due diligence that actually require human oversight.

These tools typically work by entering business identity information (like business name, address, or EIN/TIN), and searching the SOS and IRS databases to verify that information matches the information in the database.

6. Conduct ongoing monitoring on your merchants after onboarding

Once a merchant is onboarded, that doesn’t mean the job is done. You should set up alerts and tracking to monitor your merchants to check for red flags that might indicate that fraud is happening on your platform. This might include transaction monitoring, checking for excessive chargebacks, or anything else that might pose a risk to the platform.

You can also set up perpetual KYB monitoring on a cadence by checking if a business’ registration status with the IRS changes, they have a lien filed against them, they file for bankruptcy, or they end up on a Watchlist.

All of these indicators can stop fraud in its tracks, or really limit the liability you open yourself up to by allowing you to act much faster than you can if you don’t have ongoing monitoring set up for your merchants.

Find out how to balance friction and fraud with onboarding risk assessments powered by Middesk.

Top 3 merchant onboarding solutions to verify customers & assess risk

These tools are all focused on risk-assessment for onboarding, and can really help you save critical time onboarding merchants at scale, without opening your platform up to fraud.

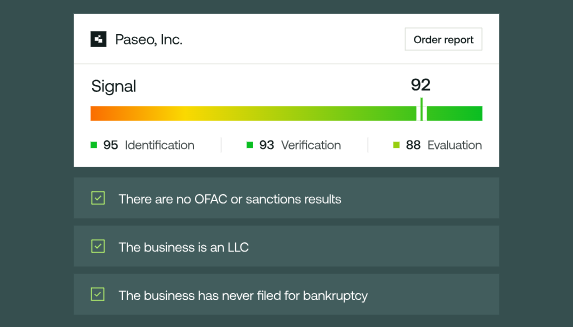

1. Middesk: best for business verification & risk-based onboarding

Middesk’s Signal product is built specifically to identify risk signals during onboarding earlier in your funnel, so you can cut out wasted time trying to dig further into merchants that are likely to commit fraud on your platform. With only 2 business information inputs (business name and address), you can immediately collect the critical business identification information you need to score the risk of the merchant.

Middesk’s Signal product is built specifically to identify risk signals during onboarding earlier in your funnel, so you can cut out wasted time trying to dig further into merchants that are likely to commit fraud on your platform. With only 2 business information inputs (business name and address), you can immediately collect the critical business identification information you need to score the risk of the merchant.

Middesk Signal will then leverage its extensive authoritative and alternative data platform to provide risk instant signals that help you determine the legitimacy of a merchant — all provided to you in a fraction of a second.

Signal will offer a score based on all the data compiled, as well as key reason codes relating to the entity type, business age, registration status, sanctions results, and more. You can set up automatic triggers for additional verifications when they are needed to move the merchant further in the onboarding process, or cut them out immediately to save further time digging into fraudulent merchants.

How it helps with merchant onboarding: Collect less information from your merchants (causing less friction in the onboarding process) by only using business name and address to score the risk of the merchant instantly.

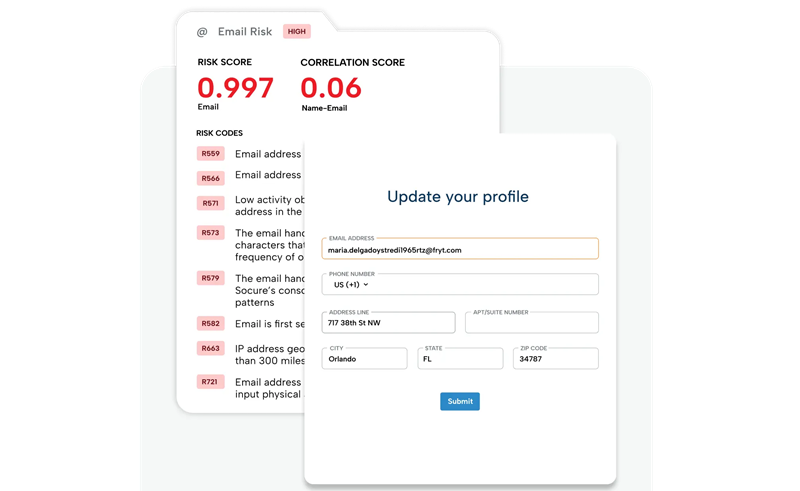

2. Socure: best for KYC

Image Source: Socure

Socure can produce a comprehensive risk score for merchants, including instant predictions on the risks associated with a phone number, email, or address, so you can identify potential threats in seconds.

In the Socure platform, you can use a drag-and-drop workflow builder to determine the order and importance of each KYC check, and you can set up real-time alerts to identify bad accounts and block bad transactions.

How it helps with merchant onboarding: You can confirm the authenticity of a merchant from a government-issued ID, match the PII extracted from the ID against the input information, and match the ID headshot to a seller-submitted selfie.

3. Sardine: best for real-time chargeback risk monitoring

Image Source: Sardine

Sardine lets you equip your merchants with custom ML models and pre-authorization rules that can stop fraud before it happens and lower your risk of chargebacks. You can also monitor your entire merchant portfolio in real-time, helping you predict emerging risks across all merchants and protect yourself from bust-out fraud.

How it helps with merchant onboarding: Set your own risk thresholds during onboarding to block high-risk merchants trying to get on the platform.

Conclusion

Middesk’s Signal & Assess tools can level up your merchant onboarding process, and help you bring more legitimate merchants to your platform at scale. Set up a personalized demo with our sales team to learn exactly how Middesk can fit into your compliance tech stack, and how it can detect risk early at the top of your funnel with only the merchant’s business name and address.