Overview

In brief:

- Digital transformation is the process of an organization adopting digital technologies to augment its current business operations or products, or create entirely new ones.

- For financial institutions’ compliance programs, that means investing in Regtech to automate compliance-related tasks and keep compliance-relevant information up to date.

- A key part of the digital transformation of business processes for financial institutions’ regulatory compliance is automating repetitive tasks, freeing up human resources for working on more complex problems.

Financial regulatory compliance is becoming increasingly complex and costly. This is partly because new technologies are laying the foundations for new methods of exchange – and new tools for criminals to abuse. An example is completely-digital onboarding for neobanks.

The good news is that financial institutions can use some of this technology to streamline their compliance operations. This helps them minimize the growing squeeze compliance puts on their time, money, and other resources.

Introducing this new technology to a financial institution’s compliance systems isn’t always simple, though. All of a financial institution’s stakeholders need to understand what they want for their business’s compliance operations, what specific technological changes will get them there, what other resources they’ll need, and how the whole process will be carried out.

This is known as a digital transformation, and in this article, we’ll explore what a successful one for a financial institution’s regulatory compliance operations looks like.

To begin, we’ll discuss what a digital transformation process is, and how it specifically relates to keeping a financial institution’s compliance system in line with its regulatory obligations.

What is the process of digital transformation?

The process of digital transformation refers to an organization adopting computer-based technologies to improve its business processes and create new kinds of products. The general purpose of doing so is to stay competitive and deliver better customer experiences in an increasingly-digital world.

In terms of financial regulatory compliance, digital process transformation revolves mainly around Regtech (regulatory technology). Because of their socio-economic importance, financial institutions are subject to complex sets of strict regulations. So manually executing all the different processes required to comply with these regulations is extremely difficult, if not downright impossible.

Also remember this includes modifying these processes to adapt to frequently-changing regulations, new product offerings, and the evolving techniques of financial criminals.

That’s where Regtech comes in. Regtech based on computers and artificial intelligence can automate tedious financial compliance functions. These include verifying customer identities, assessing client risk levels, monitoring for unusual transactions (or patterns of them), and filing suspicious activity reports. This has many benefits, from reducing human error and non-compliance risk to freeing up time and money for prioritizing tasks to grow the business.

Businesses can’t make an effective digital transformation if they don’t have reliable data to build upon. That’s why we recommend doing a rigorous KYB vendor test to ensure the data you’re getting will meet your standards for compliance and risk management.

7 digital transformation process steps to become compliant

Digital transformation is a broad concept that isn’t “one size fits all”. Each organization has different reasons for doing it – such as a financial institution modernizing its regulatory compliance program – and may start from different positions.

However, there are a number of digital transformation process steps that are common across many organizations’ plans. The following is a general 7-part framework.

1. Base a plan on the organization’s objectives and targets

The first part to building a digital transformation process model is understanding why it’s necessary in the first place. What does a financial institution hope to do by digitally transforming its compliance program? Give customers smoother onboarding experiences? Minimize operational risks? Reduce false positives to let a compliance team focus on higher-priority investigations? Free up resources for other business functions?

Each financial institution has different priorities and starting capabilities (the latter we’ll discuss in more detail shortly). So knowing where a financial institution wants to get to through its compliance business process digital transformation is one part of drawing a roadmap for it.

2. Assess the organization’s current digital technology situation and needs

The next part of the journey is to take stock of what digital technology solutions the financial institution already has. That includes what value those tools provide for the financial institution, as well as where there are gaps in the financial institution’s compliance system that digital technologies could help fill.

There are a couple of things to keep in mind here. One is the financial institution’s current available resources. Adopting digital technologies costs time and money, so being too ambitious with a digital transformation strategy can actually wind up hurting a financial institution from both competitive and financial perspectives. The financial institution may need to scale back its goals to more reasonable benchmarks, or else find ways to acquire the extra resources it needs.

Another thing to consider will help with this problem: if and how the financial institution implementing a particular digital technology in its compliance system contributes to a stated overall goal. This will help the financial institution adopt only the technologies it really needs without wasting resources on solutions for areas it already has covered.

3. Choose the right leaders, and get them involved in the process

Digital business process transformation is about more than just technology. It’s about a cultural shift in how an organization operates, and that needs to start from the top. So a financial institution needs to have managers who are willing to put in the time and effort to not only develop a digital transformation plan, but also sell the virtues of it to stakeholders – through periodic meetings, for example.

At first, meetings should discuss the findings of the first two steps: what the financial institution hopes to achieve by digitally transforming its compliance processes (and why), what it already has in place towards those ends, and what still needs to be done. Once the digital transformation plan is in the design and implementation phases, check-in topics should turn to what progress is being made, how change is benefiting the financial institution, and what’s next on the agenda.

The goal is to secure buy-in from stakeholders as early as possible so that the digital transformation change management process goes smoothly with minimal resistance.

4. Structure the digital transformation process into manageable steps

Digital transformation of a financial institution’s regulatory compliance shouldn’t be a rush job. Doing so can lead to pushback from employees, as well as sloppy process implementation that can create the very compliance risks a financial institution is trying to avoid.

It’s better to focus on a single area first – for example, automating KYC (Know Your Customer) and KYB (Know Your Business) checks with identity verification software – and implement change gradually before moving onto the next item.

There’s another benefit of rolling out digital compliance transformation in stages, too: it allows for the flexibility to pivot if a new system isn’t working the way it should. This is much better than finding a problem once all the interconnected parts are in place. At that point, major disruptive changes – or even starting over from scratch – may be needed.

5. Acquire any needed human resources

Digital transformations naturally involve cutting-edge technologies. So one of the biggest hurdles to a process of digital transformation is not having staff who understand how the technologies work and can pass that knowledge on to other employees. So a financial institution should address any shortcomings in terms of training and personnel, either with regulatory compliance itself or the latest KYB solutions.

There are a few different ways to do this. One is to hire employees with specialized expertise; make sure they are learning-focused, open to ideas, and adaptable. Another is to partner with the company (or companies) whose KYB solution(s) you’re adopting, and have them run comprehensive training programs with your employees. At the end of the day, be sure to choose a KYB solution that fits your needs and expectations.

6. Encourage collaboration and feedback

Again, a reason to implement a digital transformation change management process in stages is to allow for making adjustments. Towards this end, a financial institution should seek regular input from employees with relevant experience – especially those on the front lines of regulatory compliance operations.

This will help to fix problems early, as well as steer the program closer to the company’s practical compliance needs and capabilities.

7. Put it all together and execute the plan

Okay, let’s recap:

- You’ve drawn up a digital transformation plan tailored around what your financial institution needs in the way of improving its regulatory compliance operations

- You’ve identified what digital technologies you already have in place for compliance, and where your compliance operations could use some help

- You’ve got both management and employees on board with the vision, and are fostering a teamwork-focused culture

- You have a plan to address any lack of compliance or technology expertise in your personnel

Now it’s time to move forward, slowly but surely. Prioritize one digital change to your financial institution’s compliance management system that closely aligns with your goals, and gradually roll it out. Choose a solution that best fits your financial institution’s specific needs, then hire and/or train personnel to fill skill gaps as necessary.

Ensure managers communicate with frontline employees to understand what’s working and what isn’t, and adjust course accordingly. When finished, move on to the next change and repeat until your compliance program’s digital transformation is complete.

Digital transformation and process automation

A core reason to digitally transform a financial institution’s regulatory compliance system is to automate repetitive tasks, which helps ensure these processes get done on time while expending fewer resources, as well as minimizing the chance of human error.

This is especially important for FIs in the case of automating the Customer Due Diligence (CDD) process and automating client onboarding.

Here are some examples of the easiest way to automate digital processes for financial institutions:

KYC, KYB, and KYE

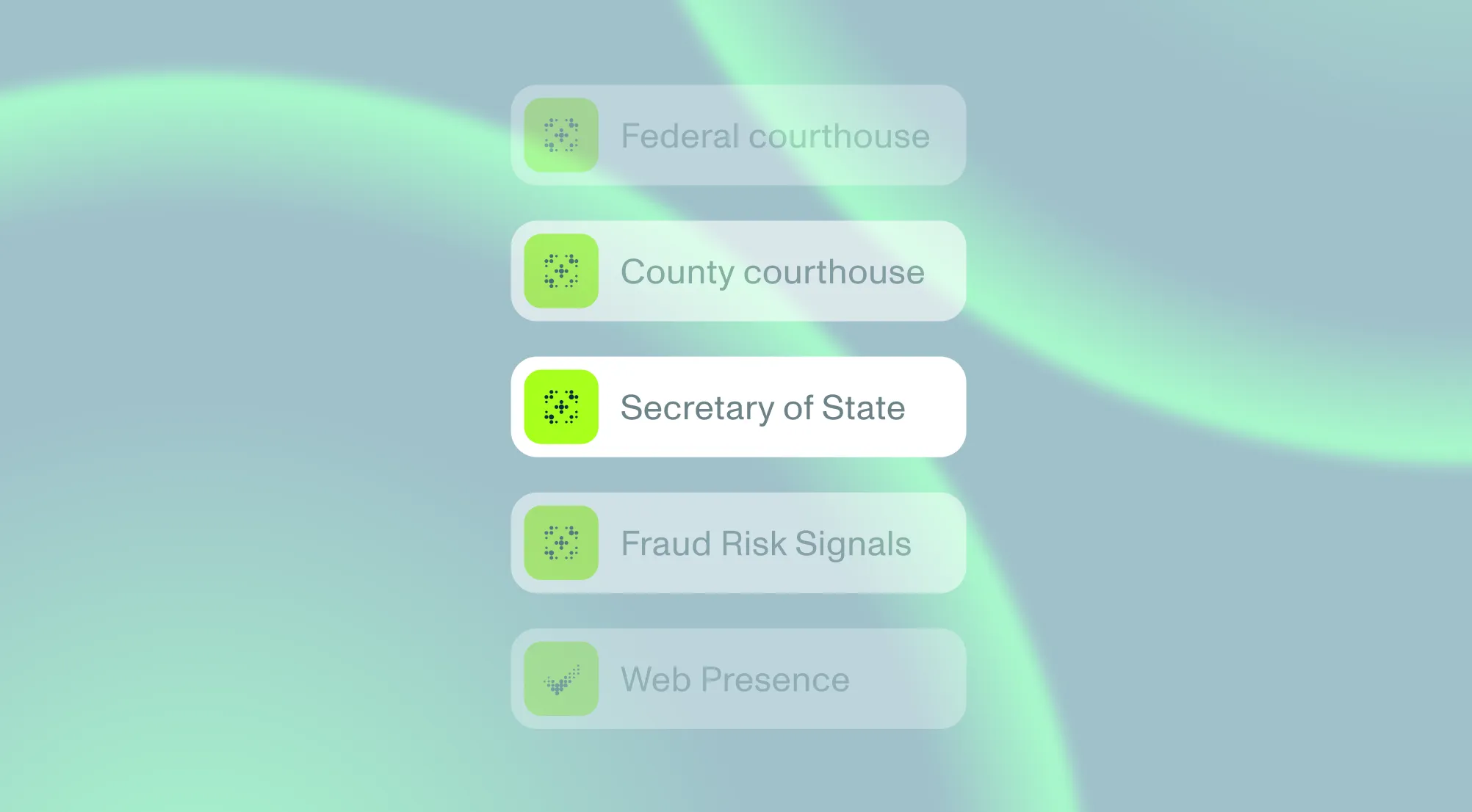

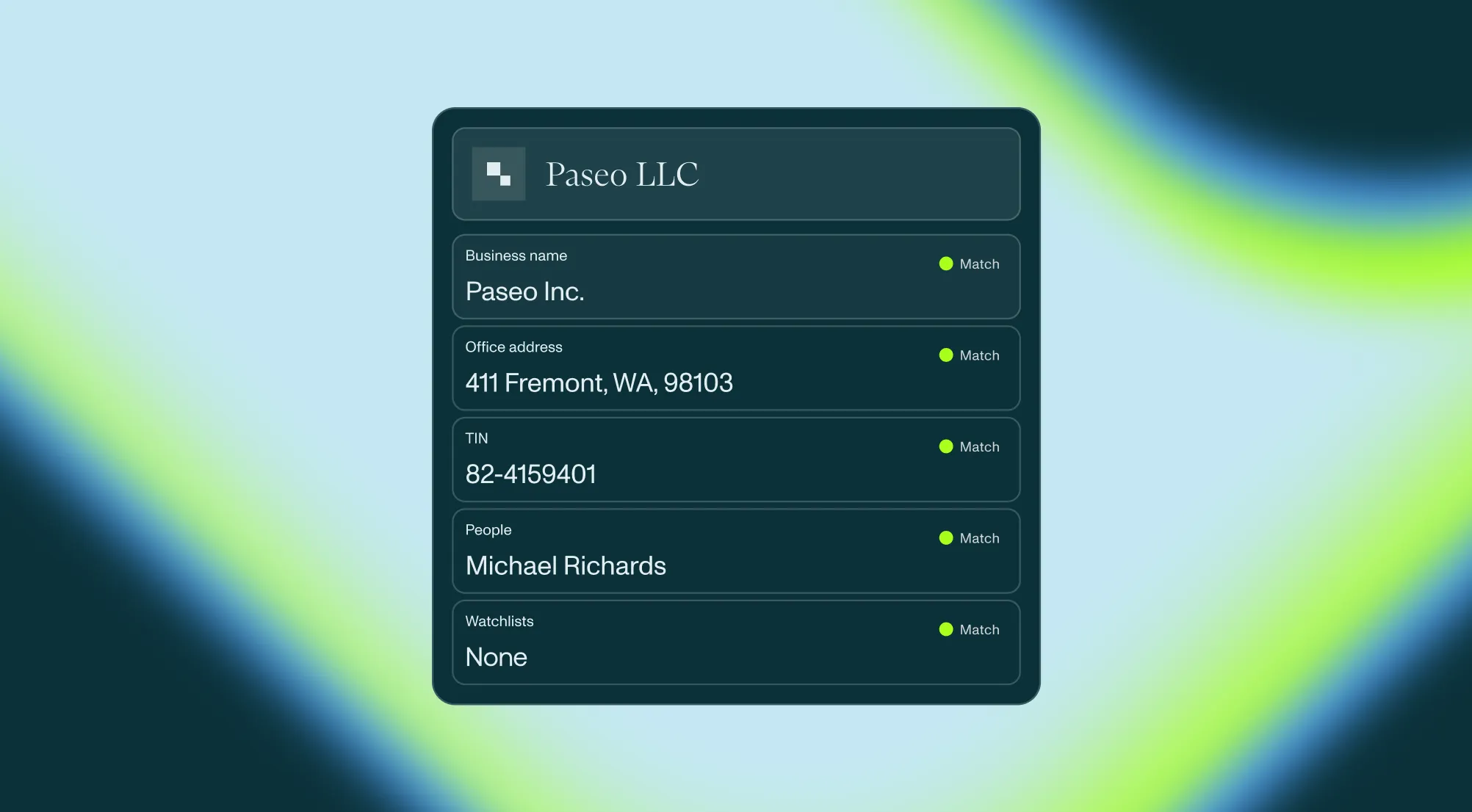

Regtech software like Middesk Verify allow compliance teams to search more data sources, faster, to find and assess identity credentials through TIN/EIN search tools on 100% of all registered businesses, and can help assess financial risk indicators associated with people and companies. This allows for safer and smoother onboarding and risk review of individual customers, business clients, and employees.

Regulations change management

Financial regulations and regulatory lists (such as sanctions lists) are altered or added to periodically. Failing to keep up with these changes can lead to a financial institution getting in trouble with governments and other regulatory agencies.

Ongoing transaction monitoring

Analyzing customer transactions is the only sure way to know whether or not they’re currently engaged in financial crime. But when financial institutions typically have thousands of clients, examining each transaction manually is virtually impossible.

That’s why financial institutions use Regtech tools – especially ones based on machine learning – to automatically scan transactions and use rules-based approaches to determine if there is anything suspicious about them.

Suspicious activity investigation and reporting

Some Regtech services provide visual link analysis of transactions and relevant contextual information. This allows financial institutions to more accurately evaluate whether unusual activity is actually suspicious or is just a false positive.

Regtech can also help financial institutions automatically file SARs and other reports with the appropriate authorities so the financial institution isn’t penalized for missing deadlines.

Case management

Regtech is also great for storing and organizing compliance-related information for later use. This includes standardized procedures for responding to incidents, reports on how specific incidents were handled, and notes on overall industry trends regarding certain types of incidents.

Having all of this information in one place allows for streamlining look-back reviews, task delegation, auditing, and coordination of anti-fraud/AML efforts.

Conclusion

In summary, digital transformation process management for a financial institution’s compliance program requires company stakeholders – from managers to employees – to understand a few things. These include:

- The overall business goals for digitally transforming the FI’s compliance operations

- Which technologies are needed (or are already in place) to achieve these objectives

- How and why the digital transformation is being done, and will improve compliance

- What training or personnel hires are needed to fill competence gaps

- What FI-specific adjustments need to be made as implementation is rolled out

To see how Middesk's Business Verification tool – or any of our other products – can be integral to your financial institution’s digital transformation, contact our sales team to set up a demo.