Overview

In brief:

- When looking for the right KYC software for your business, you should consider your AML compliance requirements, your clientele’s size and overall risk profile, what data you’ll need for ID verification & risk assessment, how easy the software is to use, specific KYC pain points you want to address, and what price a business of your size can afford.

- To be effective, KYC software should have strong data security & privacy, many time-saving automations, the right amounts and types of data to properly verify customer IDs and create risk profiles for them, an easy-to-use interface that integrates with tools you already use, and customization options that let you fine-tune it to meet your business’s specific needs.

- Using software for KYC is better than not because it lets you check more data sources, screen faster, avoid mistakes by automating tasks, give (or even implement) automatic updates, customize it to target your most critical KYC issues, and generally free up your compliance team to work on higher priorities.

Financial institutions and other money services businesses have been required to perform Know Your Customer since the 1970s, after the passing of the Bank Secrecy Act (BSA) — but it’s been over 50 years since then. New technologies and financial services have emerged – but so have new ways for criminals to abuse them to pull off fraud schemes, launder money, and commit other illegal financial acts.

FIs are expected to move just as quickly to guard against financial crime, and that’s only possible if they have the right Know Your Customer software. This article serves as a guide for finding the software platform that’s right for your business.

We’ll dive right into things by covering factors you need to consider when deciding which KYC software system is most ideal for your business.

How to choose the right Know Your Customer software for your team

There are many KYC programs on the market, so it can be hard to know where to start in choosing which one your business should use. We’ve put together a list of 6 key considerations when deciding on what KYC software program to go with, including questions to help you think about each factor in more detail.

1. Compliance obligations

Obviously, you need to keep in mind the AML rules you have to follow and whether your KYC compliance software is equipped to handle them.

Questions to ask:

- What regulations do you need to comply with on industry, regional, and international levels?

- Does a software have presets that match your compliance requirements, or do you have to set most of this up manually?

- Can the software automatically update to match requirements as they change, or at least alert you to these changes so you can make adjustments?

2. Clientele size & risk

How many customers you have, paired with how risky they are (from a financial crime perspective), is another thing to think about in terms of your company’s overall risk appetite.

Questions to ask:

- How many customers does your company have now, and how many do you forecast having at some point in the future?

- How many customers do you typically gain or lose over a measured time period?

- What is the highest level of risk among all of your customers?

- On average, are your customers normally low-risk, high-risk, or somewhere in between?

3. Data requirements

You’ll need different datasets based on your customers’ risk levels, as well as the specific reasons why they’re risky. Here are some questions you should consider about those and a KYC verification software’s ability to provide them.

Questions to ask:

- How many data types are needed to balance sufficient KYC procedures with minimizing friction on customer processes (especially onboarding)?

- Where does the software get its data from, and are these sources credible?

- How often does the software refresh its data to keep things up-to-date?

- Does the software offer a combination of authoritative data (like the SOS & IRS databases), as well as alternative data (like adverse media screening, online footprint and web presence, or IP address behavior)?

Did you know? Middesk’s has some of the freshest data in business identity verification, with 92% of business records updated within the last 10 days for 100% of registered businesses in the U.S. We also use a combination of alternative and authoritative data in our software, which enables a comprehensive approach to KYC for businesses.

4. Ease of use

Even the highest-performing KYC software won’t do much if your risk team members don’t know how to use it properly.

Questions to ask:

- How complicated is the software to learn, and do your risk team members have the necessary skills and qualifications to learn it?

- How long will it take to train your team on the software, and how will you deal with your business potentially being vulnerable to AML compliance issues in the meantime?

- How much support does the vendor provide? Do they offer group training, one-on-one coaching, or both? Do they offer dedicated customer support if you need help or something goes wrong?

5. Company-specific KYC pain points

Various factors can affect which aspects of KYC compliance your business is good at and which need reinforcement. Do an internal audit to figure these out.

Questions to ask:

- Which areas of KYC – and AML compliance as a whole – are your business already well-prepared in, and which ones could use improvement?

- What are the most common and the most dangerous financial crime threats your business faces on a day-to-day basis?

- Does the KYC software you’re assessing have customization options that let you fine-tune it to focus on covering your business’s KYC/AML weaknesses?

- How much will this tool help automate client onboarding, and how much efficiency can I expect from it? How will I measure this?

6. Company size and AML compliance budget

Though you probably wish your business had an unlimited budget for KYC software solutions and other AML compliance tools, it doesn’t. So you have to choose an option that’s appropriate to both your business’s size and what it can afford.

Questions to ask:

- Does the software seem inherently designed for a certain size or type of business?

- Does the vendor offer tiered pricing plans, letting you choose which features and price point fit your business’s size and other needs?

- Can the software scale to adapt to your business gaining a larger customer base or branching out into other services?

Now that you know some things you should keep in mind when picking the right KYC software for your business, let’s look at what features are going to fill those needs.

5 critical KYC software features to look for in a quality solution

What’s important to your business in a digital KYC platform isn’t always going to be the same as what another similar business prioritizes. With that said, there are some core features that you want to look for when you’re shopping for the right KYC program for your business.

1. Strong data privacy and protection

Your customers should be able to rest assured that the PII and other information used to perform KYC checks on them isn’t ending up where it shouldn’t be or being used for the wrong purposes.

Your KYC management software should have solid security and encryption protocols, including intuitive access controls. This helps to ensure data isn’t stolen from the outside or leaked from the inside.

2. High level of automation

One of the most powerful things software can do is automate the Customer Due Diligence (CDD) process, as well as other processes in Know Your Customer checks. Data retrieval, ID verification, risk measurement, and ongoing compliance monitoring: as much as you can get your to competently handle the jobs that make up these processes, you should.

Every task you automate means less time and money you have to spend on having your risk team members do it manually, less chance of a mistake due to human error, and more time for your risk team to work on higher-priority tasks.

3. Proper data for thorough ID verification and risk analysis

Make sure your software vendor has access to all the data you need to fit your business’s risk appetite in conducting KYC. You need the right data to do complete ID verification and adequate customer due diligence.

This due diligence can include sanctions list and other watchlist matches (like checking a person against U.S. OFAC lists), politically exposed persons (PEPs) and relatives & close associates (RCAs) list matches, and screening for adverse media coverage in the news or on social media.

You want your software to be able to pull data from many different sources, as this lets you get a consensus on whether a person’s ID information and risk signals are valid or not. But you also have to pay attention to which sources you’re getting data from, and ask if they’re credible enough to likely be giving accurate information.

Finally, you should ask KYC software vendors about how often they re-check or “refresh” their data sets so you know how soon you’ll be able to get the most up-to-date data. If you need help judging the quality of data you’re getting from a software vendor, our article below on running an effective KYB (Know Your Business) vendor test should give you a good starting point.

Learn how to run an effective KYB vendor test so you can find the ideal fit for your team.

4. Ease of use, including integrations with familiar tools

You want your KYC software to be simple enough to learn that your risk team can set it up and start using it without needing a lot of time, effort, and coaching. The sooner you get the software up and running, the sooner you’re protected against compliance vulnerabilities.

What also helps is if the software is able to integrate with other programs and systems your business already uses. That way, your risk team members can continue using interfaces they’re already familiar with instead of having to learn new ways to do the same tasks.

5. Customizable functions you can tune to your business’s unique needs

KYC software is often designed for a number of different use cases, so it includes pre-built rule sets that give many types of businesses a head start in setting up their compliance systems. Be sure to ask if your business is one of those covered!

Beyond this, even businesses in the same industry can be in different scenarios based on their location, size, clientele, and other variables. Your business may encounter a particular problem (such as money laundering) rarely, but the same problem might be a common challenge for a similar company because of its specific situation.

You should be able to adjust your KYC software to account for these differences. This lets your business be better-equipped to handle the issues most relevant to your situation, instead of being stuck with a one-size-fits-all solution that treats every part of KYC the same way.

Top 5 KYC software vendors & solutions for business identity verification

What makes the best KYC software is going to mean different things to different businesses, depending specifically on what type of identity verification you are completing. We think these 5 are solid all-around options for a variety of use cases.

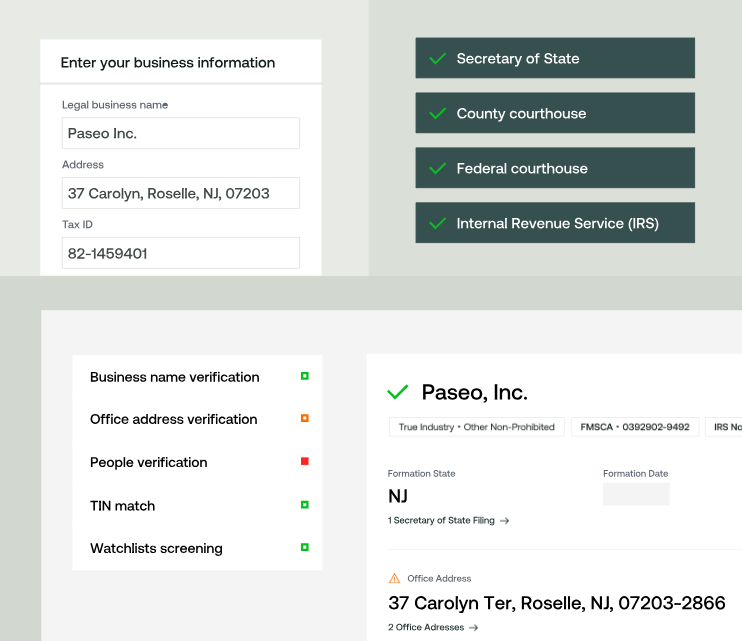

1. Best for corporate KYC: Middesk

Best for: Performing comprehensive KYC for businesses in the U.S. to verify them before onboarding.

Middesk is a corporate KYC, or Know Your Business (KYB) platform that’s also able to do regular KYC through its integration with Socure. Middesk’s data comes directly from U.S. government agencies and other trusted sources, and is refreshed frequently so you know sooner when someone’s identity details change.

It works best for identifying and assessing the risk of notable people tied to U.S. businesses, including finding businesses’ ultimate beneficial owners (UBOs). It can tell if they’re on sanctions lists or other watchlists, are in exploitable political positions (or related to someone who is), being portrayed negatively in news or on social media, and more.

Don’t just know about the businesses you deal with – know about who’s behind them too with Middesk’s KYB software.

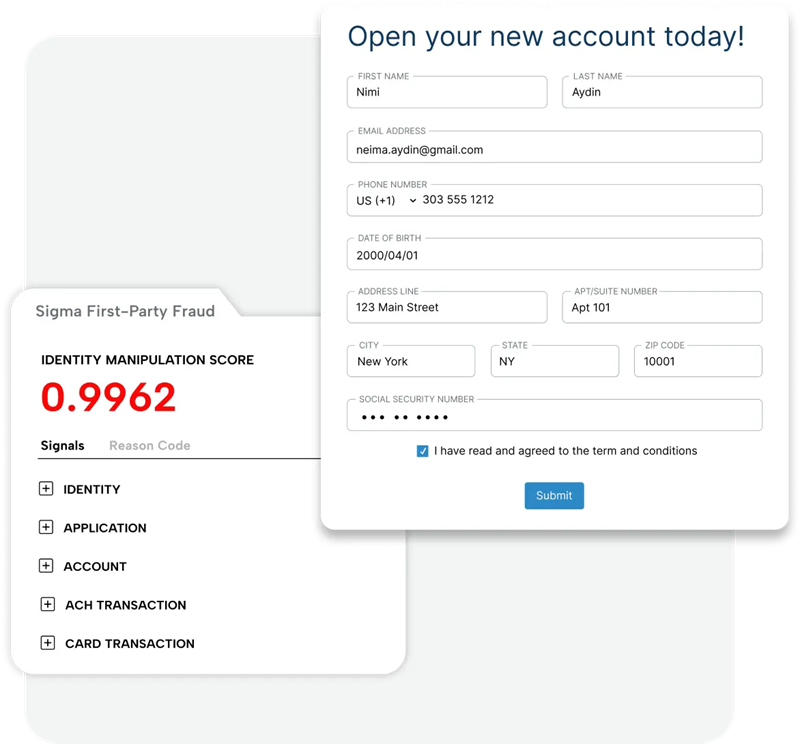

2. Best for customizability: Socure

Best for: Creating and testing custom workflows to optimize your KYC platform for your particular business

Socure’s RiskOS system is a powerful piece of software that allows you to build, test, and fine-tune your automated KYC processes. Start with ruleset templates and add over 50 different categories of data to check, and test your creations in the background without compromising your current KYC system. And you can do it all without knowing how to write computer code!

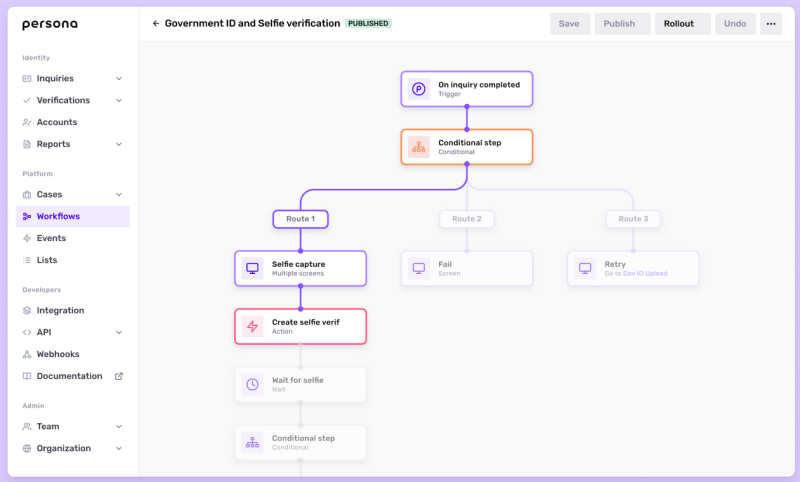

3. Best for ease of use: Persona

Best for: Intuitive but powerful KYC controls suited to a number of different use cases.

Persona’s AML/KYC software provides simple, no-code KYC interfaces and controls that are still very effective. It consolidates customer ID & risk information, relationship link analysis, verification workflows, and follow-up actions into a single dashboard. Persona’s ease of use makes it suitable for a wide variety of use cases.

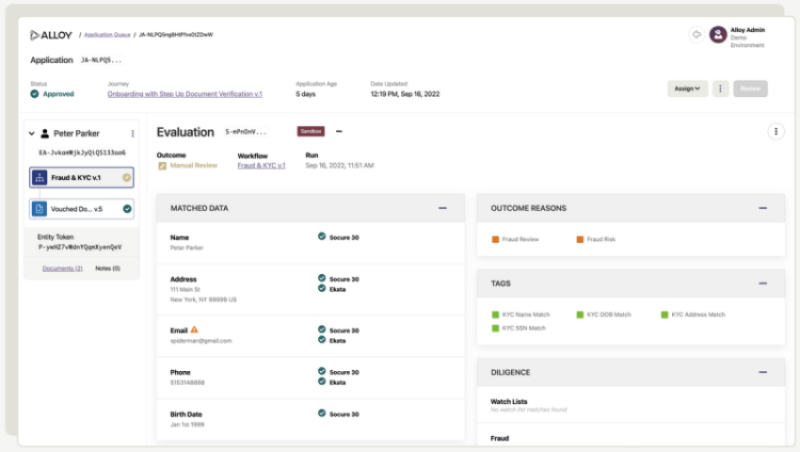

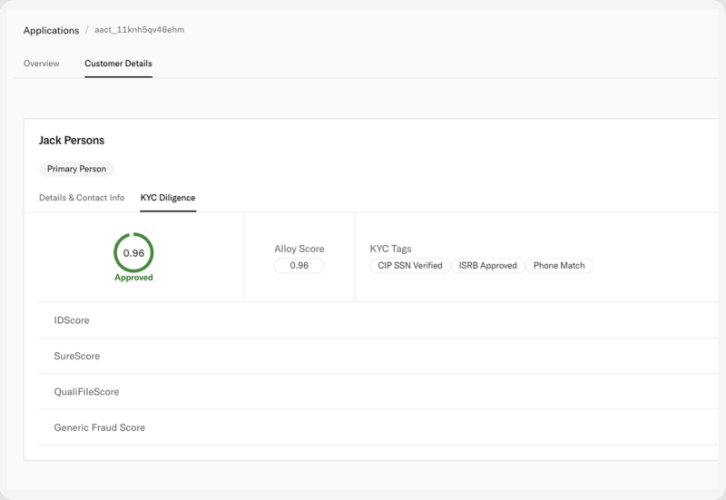

4. Best for ongoing monitoring: Alloy

Best for: Maintaining tight surveillance over high-risk customers.

If you need your identity and transaction monitoring for KYC to be as close to real time as possible, Alloy’s KYC onboarding and continuous monitoring software might be for you. When you create customer identity and risk profiles, Alloy uses its unique “data orchestration” system to bring together data from over 200 trusted sources to verify and evaluate client details. These profiles automatically update if information changes, and automatically adjust their risk scores depending on what categories of information you do or don’t check for in your KYC workflow.

5. Best for complete bank management: Treasury Prime

Best for: Financial institutions that need not just KYC, but complete management software

If you want to comply with your AML obligations AND keep the rest of your bank running smoothly, you don’t need multiple pieces of software. You need Treasury Prime’s KYC software for banks.

In addition to bank management tools, Treasury Prime has KYC functions such as custom onboarding and risk assessment workflows, real-time ongoing customer monitoring, and automated reporting functions. And if Treasury Prime’s KYC isn’t quite enough for your business, integrate over 20 other KYC tools to shore up the areas of your KYC program that need help.

Top 6 benefits of using an effective Know Your Customer software

The right software helps you streamline your business’s AML compliance processes by accelerating and automating tasks that would simply take up too many of your resources – especially time – if done manually. Here are 6 examples of how it does that.

1. Allows for checking a greater variety of data sources

Software gives you the flexibility to consult many more data sources faster than you could manually. This lets you verify more types of customer ID information, and cross-check this information against multiple sources to ensure it’s valid. An example is a Secretary of State API solution, which lets you quickly check for information in all U.S. Secretary of State offices at once.

2. Speeds up screening, reducing friction

A computer program can analyze and match ID information faster than humans can manually. Likewise, it can also do initial risk assessments based on this data quicker. This allows you to run KYC checks on customers more rapidly without them needing to provide excessive amounts of ID information or wait long for approval.

3. Automates tasks to avoid mistakes

There’s a lot you have to do for KYC:

- Find and retrieve data to check a customer’s ID information and risk level against

- Check the ID information against each data source to ensure the data lines up

- Check each source for risk factors relative to the customer

- Calculate a risk score for the customer based on the types and severities of their risks

- Decide, based on the customer’s risk score, whether or not to onboard or retain them

- Develop a risk-based, real-time compliance monitoring plan for an onboarded or retained customer

All of these processes are made up of several subtasks that, while tedious, are vulnerable to human error and can cause costly misinformed decisions if not done right. But well-programmed software can automatically take care of many of these tasks faster than your compliance team can do them manually, and with virtually no chance of mistakes.

4. Frees up your compliance team for other tasks

Another benefit of having software automate and speed up repetitive KYC tasks is that you don’t have to spend human resources on getting them done. That means your risk team has time to work on more complicated cases that need manual reviews and judgment calls, or even to help with work that grows your company.

5. Automates updates, or at least notifies you of them sooner

KYC compliance is an ongoing process, so you have to adapt when things inevitably change. Customer ID or risk-related information could change suddenly (perhaps even suspiciously), and regulatory requirements are updated frequently as fraud trends come and go.

Your KYC software should be able to keep track of these changes and update your systems accordingly, or at least give you instant alerts so you can address these changes quickly and not fall behind.

6. Customize the software to your business’s unique needs

Good software for KYC implementation is built to cover a wide range of use cases. So it also tends to include customization options that let you fine-tune how it works towards your business’s specific situation.

For instance, if your business has to follow regulations specific to your industry (such as lending or insurance), the software is bound to have rule presets you can use to hit the ground running. Or, if your business faces certain types of threats more than others, you can calibrate the software to have your detection rules be looser or stricter.

Many KYC programs also integrate with other commonly-used software. This means you don’t need to buy a KYC platform that does absolutely everything you need but costs a fortune. It also means you can keep using the interfaces you’re already familiar with.

6 important Know Your Customer software FAQs answered

Here are a few other things you should know or consider when shopping in the Know Your Customer software market.

1. What is KYC software, and what is it primarily used for?

KYC software is a web-based tool that enables the Know Your Customer process. It speeds up and enhances tasks that are part of identity verification and risk assessment – the two key parts of KYC – sometimes automating these tasks outright and cutting down on manual reviews and internal company resources.

When implemented successfully, KYC software saves spending excessive time, money, and human effort on maintaining AML compliance manually, which would tie up resources needed for other activities within a company.

KYC banking software is primarily used by financial and finance-related institutions – such as banks, fintechs, lenders, insurers, marketplace managers, and payment processors – to protect their services from being defrauded, used to fund bad actors, or otherwise abused. It helps them check a wide variety of trustworthy information sources very quickly to see if a customer’s identity and risk-related information are credible. It can also help them calculate an overall risk score for a customer based on the type and severity of risk signals found about them.

2. What type of tech is used in KYC software and how does it work?

Much of the technology in AML/KYC compliance software is based around two processes: data matching and decision-making. Data matching verifies customer ID authenticity against other sources, using methods like character recognition, biometrics, facial recognition, and liveness detection. Lookup tools cross-reference ID information with official records for consistency.

Decision-making involves quantifying or qualifying potential risk from customer information, including missing or mismatched data. Risk is determined by the exactness of information matches and category weighting. The second part is deciding action based on assigned risk. For example, the software can streamline onboarding by automatically approving low-risk customers while rejecting those that are too high-risk. Ambiguous cases might trigger further checks or manual review.

There are a few categories of technology that can be used in KYC programs. A common one is rule-based decision-making, where a customer identity or transaction case moves through a workflow based on what criteria it does or doesn’t meet. Another is big data analytics, where the software analyzes massive amounts of KYC data for patterns that make it easier to spot hidden risks or invalid ID information. Similarly, artificial intelligence can retrain itself based on a business’s past KYC case outcomes and patterns to make better decisions in the future.

Find out how conducting onboarding risk assessments can help you balance friction and fraud.

3. What types of businesses benefit from using Know Your Customer software the most?

KYC AML software is most useful for any business classified as a financial institution under the Bank Secrecy Act (BSA), as these businesses are legally obligated to conduct KYC. These include:

- Traditional banks

- Fintechs

- Lenders or finance companies

- Payment service providers

- Insurance companies

- Stockbrokers

- Currency exchanges

They also include certain marketplaces that deal in high-value items or services, as these marketplaces can be used to launder large amounts of money at once. That is, a criminal can buy something valuable with dirty money and then re-sell it for clean money. Such marketplaces include:

- Casinos and other gambling services

- Dealers of precious metals, stones, or jewels

- Travel agencies

- Vehicle dealerships (including airborne and waterborne vehicles)

- Real estate agencies

- Pawn shops

4. Should those businesses build or buy Know Your Customer software?

Some businesses may prefer to build their KYC systems in-house rather than buy software from third-party vendors. They may think proprietary solutions will offer greater customization and flexibility, allow them to keep greater control over their data, or be less expensive to implement. And they may be right – at least at first. However, there are risks to this approach.

In-house KYC platforms typically require large upfront investments of human resources, money, and especially time. In addition, a company that uses one is wholly responsible for any system maintenance and data/regulations updates; this is a further expense. And even still, the platform may still not perform as well as any third-party solution on the market. Or even if it does, it’s likely costing the company much more than initially anticipated.

Buying a third-party KYC platform can mean trusting someone else with all the back-end stuff – security, updates, data storage, and so on. But the upside is you don’t have to devote resources to doing those things yourself. Plus, you get a KYC-specific tool that’s ready right out of the box, easier to scale, and has more predictable pricing with monthly or annual rates.

5. Is KYC software worth the price?

While KYC software may seem expensive, it’s worth the money because it saves you a lot of headaches in the long run.

Manual KYC takes up a great deal of your compliance team’s time, which also leaves your customers in the lurch and frustrated. Furthermore, it carries a greater risk of human error which could lead to losing customers, onboarding bad actors, and wasting even more time. Not to mention that regulations and fraud trends tend to change very often, making it difficult to keep up with these changes if you’re doing everything without digital help.

KYC software prevents these problems by digitally automating tedious tasks so they’re done faster and with a much lower chance of mistakes. It also speeds up ID verification by cross-checking ID information against multiple sources at once, instead of one at a time. Finally, it simplifies analyzing and adapting to changes in fraud patterns and compliance rules.

All of this leads to more time and money available for your compliance team to work on complex KYC cases or revenue-generating projects. Meanwhile, it avoids costing you money from fraud, lost customers, and regulatory penalties.

6. What are the main information points KYC software should tell me about a business?

Conducting KYC on businesses is often called ‘corporate KYC’ or ‘Know Your Business (KYB)’. From a strictly KYC perspective, software needs to identify a business’s ultimate beneficial owners (UBOs) – the people with the most control over or most to gain from a business. It should also confirm, at minimum, the following information is valid and unique to each identified UBO:

- Full name

- Home address

- Date of Birth

- A number from a piece of government-issued ID

On the business side of things, the software needs to check that the following information, at minimum, is valid and unique to the business:

- Legal name (not its ‘doing business as’ name)

- Operating address (not its registered address)

- Tax identification number (usually an Employment Identification Number, or EIN)

- Registration documents (articles of incorporation, partnership agreement, etc.)

- Any required industry-specific licensing

In addition, to judge how risky the business is, the software should be able to find and analyze risk-related information on both the business AND its UBOs. This includes:

- How financially healthy they are, and how often they make big money moves

- Patterns of strange and complicated money moves with no apparent financial purpose

- Patterns of using foreign banking, private banking, or other high-risk banking methods

- Presence on a sanctions list or other watchlist, or operations in a country that’s on one

- Any significant negative media coverage on either an UBO or the business as a whole

- If any UBOs are politically exposed persons (PEPs), and what risk that represents

Middesk can find all of the information above (and more!) so you get a clear picture of whether a business is legitimate and its UBOs aren’t involved in anything shady.

Speed up customer onboarding risk assessment with Middesk KYC software

Meeting strict AML compliance requirements shouldn’t mean slowing down onboarding and verification processes until customers get impatient or potentially abandon them. Middesk’s Socure integration adds KYC to KYB so you can check if a business is legitimate, as well as the people behind it.

Try out our Verify, Signal, TIN Match, or Assess products by contacting our sales team for a demo of whichever ones you want to see in action.